SMM January 13: From the perspective of macro factors, China's display production in 2024 is expected to show an overall growth trend. According to market research institutions, China's standalone monitor market shipments in H1 2024 are approximately 10.5 million units, with stable YoY performance. Additionally, IDC forecasts that China's PC monitor market shipments in 2024 will reach 27 million units, up 3.3% YoY. The overall positive outlook for the display industry ensures demand for ITO targets.

Fundamentally, from the supply side, Q4 domestic production and supply remained stable. In China, as the zinc industry continues to operate at full capacity, the supply of by-product indium will not face short-term shortages. However, with the decline in the supply of indium-containing materials, the overall indium production in 2024 is expected to show a downward trend, with an estimated market production of approximately 960 mt.

Demand side, with the arrival of the traditional off-season in the indium market in Q4, domestic end-use demand saw a significant decline compared to Q2 and Q3. Various end-use sectors held a bearish view on indium prices, purchasing raw materials as needed with weak stocking intentions. Overall, the 2024 ITO target market demand is estimated at approximately 480 mt, with slight MoM growth but relatively small in magnitude. Indium compounds are estimated at about 40 mt, also with slight growth. Solder alloys are around 15 mt, remaining stable. PV thin films are approximately 20 mt, with slight growth. Other fields, including heterojunction batteries, are estimated at about 110 mt. Speculative demand, however, has significantly weakened.

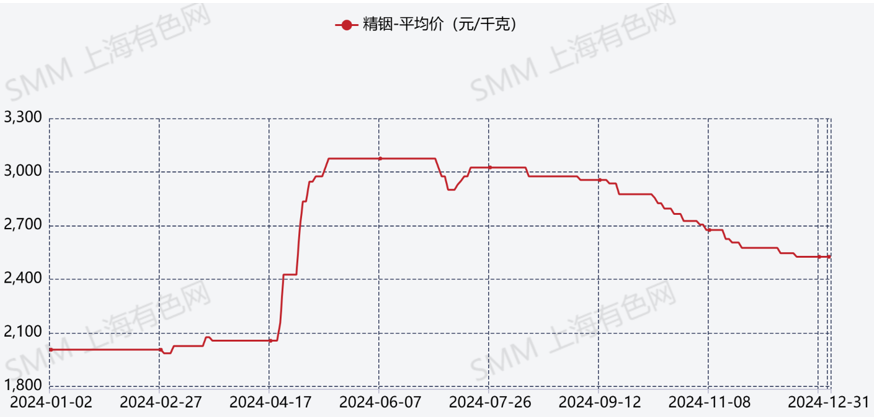

From the perspective of imports and exports, customs data for January-November 2024 shows a net export of indium-related products of approximately 286 mt. Therefore, from a fundamental perspective, the current indium market is in a relatively balanced state of supply and demand, with supply slightly exceeding demand. As a result, indium prices have remained high. However, with demand softening slightly near year-end in Q4 and the reduction in speculative demand, prices have shown a downward trend.

From a price perspective, prices reached their annual peak in Q2, exceeding 3,000 yuan per kilogram. Starting in Q3, prices showed a weakening trend, with the downward slope increasing in Q4. By December, prices stabilized again at around 2,500 yuan per kilogram. One of the main influencing factors on prices remains speculative capital involvement in some forward transactions, which has had a certain impact on spot prices.

Market trends indicate that, given the relatively mature fundamentals of the indium market, future supply changes are expected to be minimal, and there are no significant growth areas in downstream demand. Indium prices are expected to operate within the range of 2,400-2,800 yuan per kilogram in the future. However, speculative capital-driven fluctuations could lead to greater price volatility.